TL;DR

- UAE businesses outgrow manual spend controls fast, and the fallout shows up as slow month-end closes, untracked cash, and stale numbers.

- Petty cash, expense reports, paper policies, and bank corporate cards still dominate, but each runs out of road.

- The new standard: Virtual corporate cards paired with spend management software put control on the card itself, in real-time.

- Pemo offers the best way to control your employee spending with our MENA-focused accounting integrations and unlimited virtual cards built for how UAE SMEs actually work.

Why is controlling employee spending hard for UAE businesses in 2026?

Running a business in the UAE in 2026 doesn't look like it did even three years ago.

SMEs are scaling faster than the systems behind them. Teams sit across Dubai mainland, free zones, and, increasingly, the wider GCC.

A single week of company spending can hit half a dozen currencies, with AED on petrol one day, USD on a SaaS renewal the next, then EUR for a supplier in Berlin and another stack of dirham receipts from a team offsite in Ras Al Khaimah.

The problem is that most businesses handle that spending hasn't kept up.

Then there's the regulatory side. Corporate tax has applied to financial years starting on or after 1 June 2023, and VAT has been a baseline expectation since 2018.

Both mean every transaction needs to be documented, categorised, and reconcilable, and both are legal requirements.

When the systems running underneath all of that are paper receipts, WhatsApp screenshots of bank transfers, and a spreadsheet that gets updated once a week, things can start to slip.

Here's what slipping actually looks like:

- An employee books a flight on their personal card because the company card is maxed out, then waits three weeks to be reimbursed.

- The finance team chases six receipts from a team offsite, finds three, and books the rest as "miscellaneous."

- A SaaS subscription renews on autopilot for AED 1,200 a month, even though the team using it left the company eight months ago.

- The CFO can't get a clean view of last month's spending until the 20th of the following month.

None of these feel like emergencies on their own.

Stack them up across a 30-person company over a year, and the picture changes: thousands of dirhams in leaked spend, weeks of finance team time wasted, and leadership making decisions on stale numbers.

The real cost of bad spend control isn't the money employees overspend.

It's the time, the closing delays, the audit exposure, and the slow erosion of trust between finance and the rest of the company.

That's the problem. Let's go through how UAE businesses actually try to solve it today:

What are the different ways UAE businesses handle employee expenses today?

Most UAE businesses lean on one of four approaches to keep employee expenses under control in 2026:

Let's go through each one in detail:

Method 1: Petty cash

Petty cash is the oldest tool on the list, and it's still surprisingly common in UAE SMEs that started small and never replaced it.

In practice, it looks like this: the office keeps a cash float in a drawer (usually a few thousand dirhams), and employees pull from it for low-value purchases like taxis, office supplies, courier fees, or refreshments for a meeting.

A spreadsheet or paper log tracks what's gone out and what came back as receipts.

For a four-person business buying a few hundred dirhams of supplies a week, it works. The setup cost is essentially zero.

The system starts to crack at the point of growth:

- Receipts go missing.

- The log gets backfilled days later from someone's memory, which means the numbers in the log stop matching the cash actually in the drawer.

- VAT visibility is patchy because not every small UAE merchant issues a tax invoice for a cash purchase, and the ones that do tend to get crumpled into a pocket and forgotten.

By the time someone in finance sits down to reconcile, they're working off incomplete paper that doesn't square with the bank account.

Method 2: Employee reimbursements

Reimbursements are the default fallback once petty cash stops scaling.

Employees pay for work expenses on their personal card, hold onto the receipt, file a reimbursement request, get a manager's sign-off, and wait for finance to send the money back.

There’s no need for new cards, no new tools, and no new accounts. That's the appeal.

For occasional spending, like a one-off client dinner or an emergency office purchase, it can be a workable system.

The system gets uncomfortable once reimbursements become the primary way your team transacts.

Employees end up financing the company on their personal credit cards. For a quick AED 200 lunch, that's fine.

For a return flight, a multi-night hotel, a supplier deposit, or an annual software subscription, it can be a real strain.

Finance, meanwhile, runs a different kind of marathon.

Reimbursement forms trickle in late, often with missing or unreadable receipts, and the follow-up chain eats hours each week.

Your books lag actual spending by weeks because the numbers only land when employees decide to submit.

Each transaction lands as a manual entry, with VAT and categorisation handled by hand.

Reimbursements still earn their place for irregular spending. However, as a default system, they're slow and quietly expensive in finance team time.

Method 3: Traditional corporate cards from banks

The third option on the list is the corporate card that your UAE bank issues alongside your business account.

Most UAE banks offer corporate credit cards as part of the business banking relationship.

Set up runs through your relationship manager: you apply, the bank reviews, and a physical card lands a few days or weeks later.

When an employee uses one, the card behaves the same way a personal credit card does, just with the company on the hook for the bill.

For one or two designated spenders handling high-value purchases, this is a strong setup.

Credit terms can be favourable, fraud protection is established, the bank statement is clean enough for an external auditor, and the spending itself counts toward your business's credit history.

The trouble comes when you try to scale the method across a team of fifteen, thirty, fifty, or a hundred people.

Card counts are usually capped per account, which means employees either share cards (a real security and compliance issue) or revert to reimbursements anyway.

Per-employee and per-category spending controls vary considerably bank by bank and are usually thinner than what's available on a dedicated spend management platform.

Direct sync with accounting software like QuickBooks, Xero, Zoho Books, or Tally is rarely built into the card itself, so finance teams still export statements and reconcile manually.

Issuing a card for a new hire can take anywhere from a few business days to several weeks.

Bank corporate cards earn a place in a mature finance stack. However, they tend to stall when you ask them to be the primary system for an entire growing team.

Method 4: Spend management platforms with virtual corporate cards

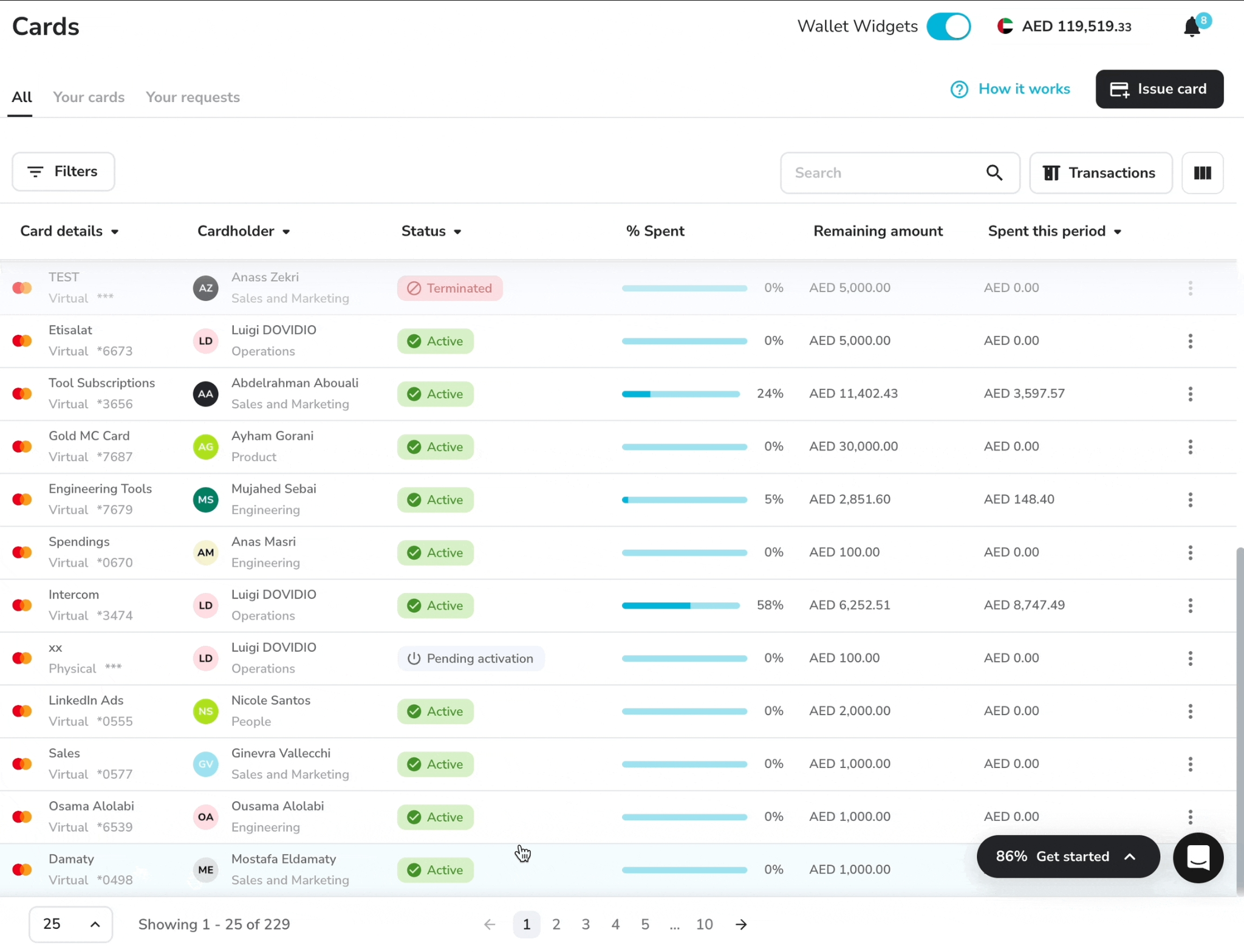

A spend management platform issues virtual (and often physical) corporate cards to every employee from a single dashboard.

Each card has its own limits and rules, every transaction lands in a live view, every receipt is captured digitally on a phone, and every transaction syncs into your accounting software in real time.

Here’s what that means for you:

- Employees no longer front cash on their personal cards.

- Finance no longer chases paper at month-end.

- The CFO no longer waits until mid-month to know what last month's numbers actually were.

The platform sits between the employee and the merchant, and the controls live at the point of purchase rather than in a PDF or a post-hoc reconciliation review.

This is the category Pemo operates in (that’s us), alongside other UAE-based and global platforms.

It works for teams across a wide size band, from a two-person startup using two free cards to a 200-person SME running a finance function with dedicated approvers.

New employees get a card from the dashboard in seconds with their own limits and policies attached.

The monthly platform cost is predictable, the spending control is tight, and the finance team time saved against the old methods typically pays for the subscription a few times over.

For UAE businesses that want to retire petty cash, end the receipt-chasing cycle, replace manual reconciliation, and close their books in days rather than weeks, this is the method that holds up.

What makes Pemo the best way to control employee spending in the UAE?

Pemo’s expense management solution offers the best way to control employee spending in the UAE with our virtual corporate cards that have real-time spending visibility, spending controls, and can be configured with an approval workflow.

Here's what it actually gives you.

Virtual Cards Your Team Can Use The Same Day

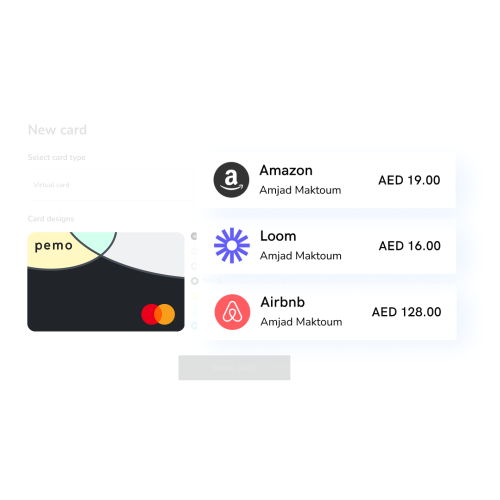

Issuing a virtual corporate card on Pemo takes seconds, not the days a bank application can run.

You log in, click create card, assign it to an employee, set the limit, and they can start spending.

Every virtual card you create is unlimited and free on the platform.

Each one carries its own monthly or per-transaction cap, its own merchant restrictions, and its own approver chain.

When an employee leaves on a Friday, their card is frozen on Friday. You don't need to call a bank, file a form, or wait for a reissue cycle to land.

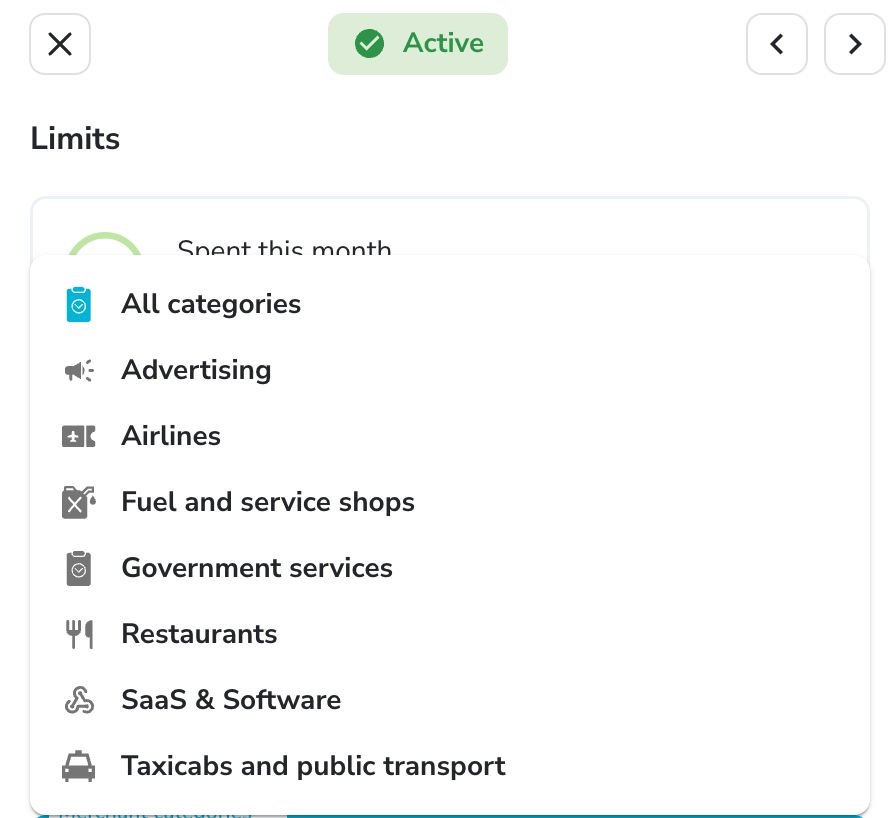

Card-Level Rules That Get Enforced Automatically

Written policies simply don't have a mechanism for this part.

In Pemo, the rules don't sit in a document. They sit on the card.

You can set marketing's monthly Google Ads budget to AED 8,000, and the card stops working at AED 8,000.

A non-approved merchant category triggers a decline at the point of purchase, not a flag three weeks later in a reconciliation review.

Approval flows run in-app, so the finance team isn't chasing managers on WhatsApp for sign-off on an AED 200 receipt.

The dashboard shows live transactions across the company, broken out by team, employee, card, and merchant, across desktop and mobile.

The CFO who used to wait until the 20th of next month for clean numbers has them in real-time.

Accounting Automation Built For MENA Finance Teams

Many spend platforms bolt international accounting integrations on as an afterthought. Pemo doesn't.

Out of the box, Pemo syncs with Wafeq (built for MENA compliance), Zoho Books, Xero, QuickBooks, and Tally.

Transactions flow into your accounting software automatically.

Pemo Copilot is the AI piece: it looks at each transaction, sorts it into the right line in your chart of accounts, tags VAT treatment, and gets sharper every time your finance team makes a correction.

VAT-ready exports come straight out of the dashboard, which matters in a market where FTA documentation requirements are part of the standard finance workflow.

Pemo's Pricing

Pemo's free Kickoff plan gives you up to 2 card users, unlimited virtual cards, single-use cards, expense management, AI receipt matching, invoice capture and payment, and accounting integrations.

For more cardholders and advanced features, Pemo has 2 paid plans:

- Essential: AED 29/month per cardholder, adds approval workflows, spend analytics, multiple wallets, advanced card controls, and 0.5% cashback on online ads.

- Business+: Custom pricing starting at 20 card users, with up to 2% cashback, a dedicated CSM, custom onboarding, priority support, and unlimited physical cards.

Want to learn more? You can sign up for Pemo's free plan or book a demo to see it in action.

How to run employee expenses on Pemo?

This is what running employee expenses on Pemo actually looks like day to day:

Step 1: Set up your Pemo account and fund your wallet

Sign-up is a few clicks.

You enter your business details, Pemo verifies your account (you can explore the platform while verification runs in the background), and then you fund your Pemo wallet via bank transfer.

The wallet is what your virtual cards draw from, which is why funding it is a prerequisite for everything else. Most UAE businesses are set up and funded within a working day.

Step 2: Issue virtual cards to your team in one click

Once the wallet is funded, you start issuing virtual cards.

Every employee can have their own, or you can structure them around purposes instead: one for marketing's ad spend, one for the ops team's subscriptions, one for a single project budget, one for your travel approver to use on company trips.

Each card carries its own limit and policy. There's no per-card fee, and you can issue as many as you need.

Step 3: Set approval policies and spending rules

Step 3 turns the card into an enforcement mechanism.

For each card or team, you set the rules: monthly or per-transaction limits, approved merchant categories, and required approver chains for any spending above a chosen threshold.

Anything that breaks a rule gets flagged or declined at the moment of purchase, not surfaced three weeks later in a reconciliation.

That's the part that traditional bank cards and written policies can't replicate together.

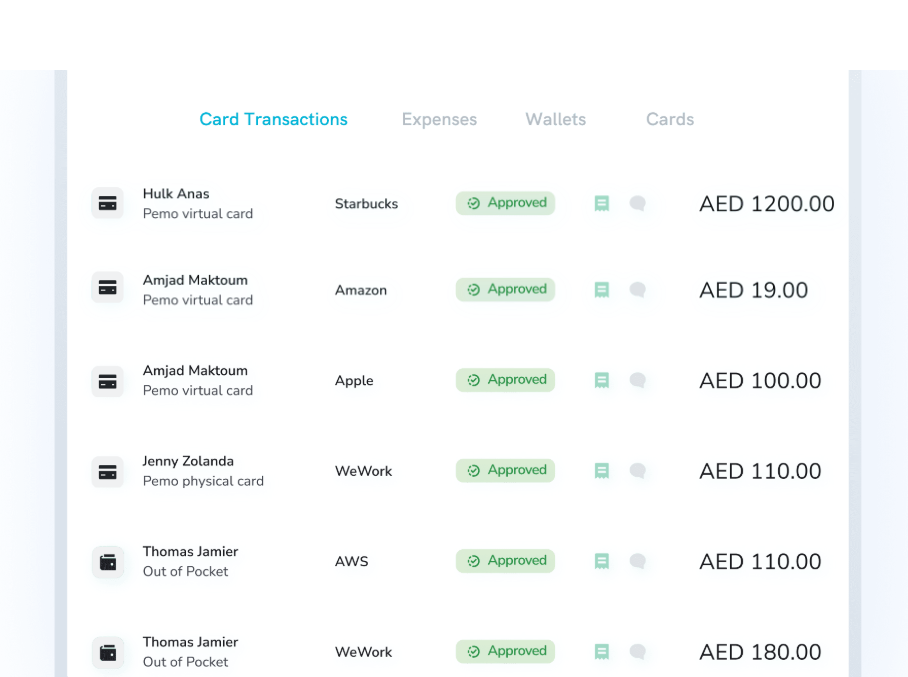

Step 4: Let employees spend and upload receipts in real-time

Employees spend the way they normally would, online or in person.

The second a transaction goes through, they get a push notification on the Pemo mobile app asking for a receipt.

One tap, photo of the receipt, done. The receipt auto-matches to the transaction in the background.

The end-of-month receipt chase from finance disappears, along with the shoebox of unsorted receipts in someone's desk drawer.

Step 5: Reconcile And Close Books Faster

At month-end, transactions are already categorised by Pemo Copilot and synced to your accounting platform.

The finance team's job shifts from data entry to review, as VAT-ready exports come straight out of the dashboard.

Get started with Pemo for free

Most UAE businesses have run on some version of cash, reimbursements, paper policies, and bank cards for years.

That's how the system has worked, and for a long time it was the only option.

The pace at which UAE businesses operate in 2026, with faster scaling, more currencies, corporate tax compliance, and multi-location teams, has outgrown what those tools were designed to do.

The teams I see handling this best aren't trying to make the old setup work harder.

They've swapped bank cards for virtual ones, replaced PDF policies with rules that live on each card, and given up the monthly spreadsheet reconciliation for a live dashboard.

If you're looking for expense management software with smart corporate cards for your UAE-based team that offers:

- Spending controls and spending approval workflows.

- Auto-receipt matching with no manual cross-checking.

- Real-time visibility into every dirham spent.

- Direct sync with QuickBooks, Xero, Tally, and Zoho Books.

Then you can sign up for the free Kickoff plan or book a demo to see why over 10,000 businesses across the MENA region run on Pemo.

Controlling employee spending FAQs

What's the best way to control employee spending in a small business in the UAE?

For most UAE SMEs in 2026, the best approach combines virtual corporate cards with spend management software.

The cards give employees the means to spend, the software enforces the rules in real time, and the whole setup syncs with your accounting platform, so finance isn't doing manual reconciliation.

You can start with Pemo’s free plan.

Are virtual corporate cards safer than physical ones?

In most cases, yes.

Virtual cards can be created for a single transaction or a single vendor, frozen instantly from your phone, and limited by merchant category.

A leaked card number is cancelled and reissued in seconds, with no courier or bank involved.

Physical cards still have their place for in-person spending, but virtual cards reduce the surface area for fraud significantly.

How do virtual corporate cards work for businesses in the UAE?

You sign up with a provider like Pemo, fund a corporate wallet, and issue virtual cards to your team.

Each card draws from the wallet, can be capped by amount or category, and processes as a regular Visa or Mastercard at any merchant that accepts those networks.

Transactions show up in a live dashboard, so finance teams have visibility from the moment a card is used.

Do I really need a separate expense management tool if I already have A corporate bank card?

For very small teams, maybe not.

Once you're past about five employees making regular purchases, though, the gap shows.

Bank cards rarely give you per-employee controls, receipt capture, automated categorisation, or live dashboards in a single package.

You can layer an expense tool on top of a bank card, but most teams find it simpler to use a platform like Pemo that handles the card and the software together.

Can I set spending limits per employee with a virtual corporate card?

Yes. With Pemo (and most modern spend management platforms), every virtual card can have its own monthly limit, per-transaction cap, and merchant category restrictions.

You can also build approver chains so any transaction above a set threshold needs sign-off before it goes through.