TL;DR

- Cash flow management is the discipline of tracking what's moving through your business and forecasting what's coming next, so working capital doesn't dry up just because the P&L looks healthy.

- Companies don't usually lose money to dramatic events. The drain often comes from uncontrolled employee spending, slow invoice approvals, books that close two to three weeks late, and the new corporate tax obligations carving cash out of every quarter.

- Pemo fixes this with prepaid virtual corporate cards that stop overspending by employees before it happens. Every transaction syncs live to your accounting software, so the cash forecast you're staring at is actually current.

What is cash flow management?

Cash flow management is the practice of watching every dirham that enters or leaves your business closely enough to know what's coming next, so you always have enough working capital to operate.

It sounds simple, but the reality is anything but that.

Most UAE founders can tell you their monthly revenue down to the dirham.

Ask them how much cash is actually sitting in the account on a random Tuesday afternoon and what's about to leave it this week, and the answer is usually a long pause followed by "let me check with finance."

That gap is where SMEs collapse financially.

Cash flow isn't about profit. It's about timing.

A profitable quarter on paper means nothing if your biggest invoice hasn't cleared and your team just expensed a conference trip nobody flagged.

In the UAE, where payment cycles run long and bank credit can be restricted for small businesses, this timing problem can hit harder than it does in markets with faster payment norms.

This is what makes proper cash flow management the difference between scaling and surviving.

Why is cash flow management so hard for many UAE SMEs?

Cash flow management is harder for UAE SMEs because the regional economy combines long payment cycles, restricted access to working capital lending, high operating costs, and a payment infrastructure where some of the company's spending still happens off the books.

The mechanics are stacked against small businesses from the start.

And operating costs in Dubai and Abu Dhabi don't pause while you wait to get your money.

The result is a structural squeeze: money comes in slow, credit doesn't fill the gap, and outflows keep moving.

Where does cash flow actually break inside a UAE SME?

Cash flow breaks in UAE SMEs at the same handful of pressure points every time:

- Poor real-time visibility.

- The company spend that finance only sees at the month-end.

- The slow close cycle that keeps your forecast stale.

- The new corporate tax obligations that catch SMEs without a buffer.

These aren't dramatic blow-ups. They're slow leaks. You only notice them when something else goes wrong.

Why don't most UAE founders know their real cash position?

The cash data in most UAE SMEs lives in four or five different places that don't talk to each other.

A Google Sheet, a bank app, the accountant's email, a WhatsApp group with finance, and a stack of paper invoices on someone's desk.

That isn't real-time visibility: that's often straight up archaeology.

What you actually need is a single dashboard, scheduled outflows for the next 30 days, live employee spending, and pending invoices updated to the minute.

Where's the company spend that finance never sees?

There's a chunk of company spend in every UAE SME that finance only learns about weeks after it happened, and it's usually bigger than founders think.

The classic spots:

- The Google Ads bill on someone's personal card, waiting for reimbursement.

- The Zoom subscription that auto-renewed annually instead of monthly.

- The client dinner at an upmarket DIFC restaurant that came in over budget.

- The driver who's been buying fuel on cash for three weeks before submitting any chits.

Each one is small on its own, but when you stack them across a 30-person team over a year, this is where the cash drift comes from.

How does the new UAE corporate tax regime squeeze cash flow?

The introduction of UAE corporate tax has created a cash flow trap that most SMEs haven't fully reckoned with yet.

Late filing and late payment now carry penalties, and the FTA has signalled stricter enforcement and audit focus as the regime matures.

Many SMEs are still building the muscle to set aside cash for tax obligations across the year, rather than scrambling near the deadline.

By the time your tax bill is due, your books should already show the cash put aside for it.

If they don't, you're scrambling for liquidity at exactly the wrong moment.

Cash flow management isn't optional in that environment. It's how you survive the bill.

How does Pemo help you control cash flow in the UAE?

Pemo helps you control cash flow by combining prepaid virtual corporate cards that stop overspending at the source, an expense management system that captures every transaction in real-time, automated invoice payments that smooth out your outflows, and accounting sync that keeps your books current to the day.

Cash flow problems in the UAE rarely come from a single failure. They come from the gap between when money is spent and when finance finds out.

Pemo closes that gap by capturing every transaction at the moment it happens, instead of at the month-end when receipts arrive in a pile on someone's desk.

Let's walk through how each piece works:

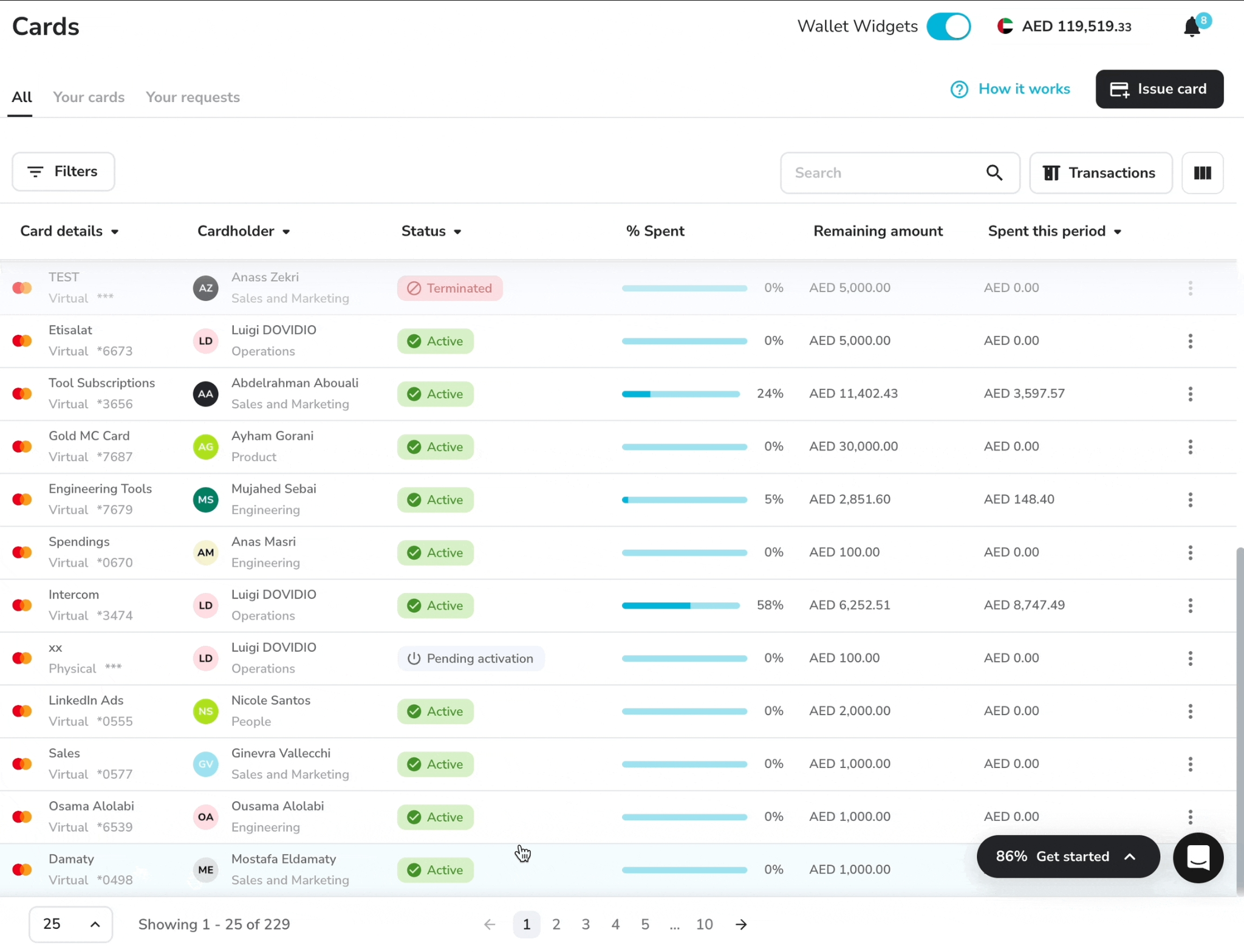

Virtual corporate cards that prevent overspending in the first place

Pemo's virtual corporate cards enforce limits before the transaction goes through, which is the opposite of how reimbursement-based expenses work.

You can issue a virtual corporate card to any team member in seconds and load it with whatever budget makes sense, such as a 5,000 AED monthly cap for the marketing lead's Google Ads.

A few specifics worth knowing:

- Spend limits: Set caps per card, per day, per week, per month, or per transaction. The card declines anything over the limit.

- Merchant category controls: It’s possible to restrict cards to specific categories like fuel, advertising, or hospitality. That means a travel card can't get charged at a software vendor.

- Instant freeze: You can freeze any card from your desktop or mobile the moment something looks off, no calling a bank required.

- Cards work with Apple Pay, Google Pay, and Samsung Pay, so nothing physical needs to ship before your team can spend.

Expense management that frees up your working capital

Reimbursements are one of the quietest drains on visibility and admin time in UAE SMEs, and Pemo removes the model entirely.

When every transaction happens on a company card, there's nothing to reimburse, nothing to chase, and no float sitting in your team's pockets waiting on payroll.

Think about how reimbursements usually work.

An employee pays out of pocket. They wait. Finance reviews the receipt. Eventually, payroll cuts or a reimbursement.

Multiply that across a 30-person team, and you're effectively holding employees' personal funds at any given time.

Plus, you're spending admin time reconciling reimbursements that should never have existed in the first place.

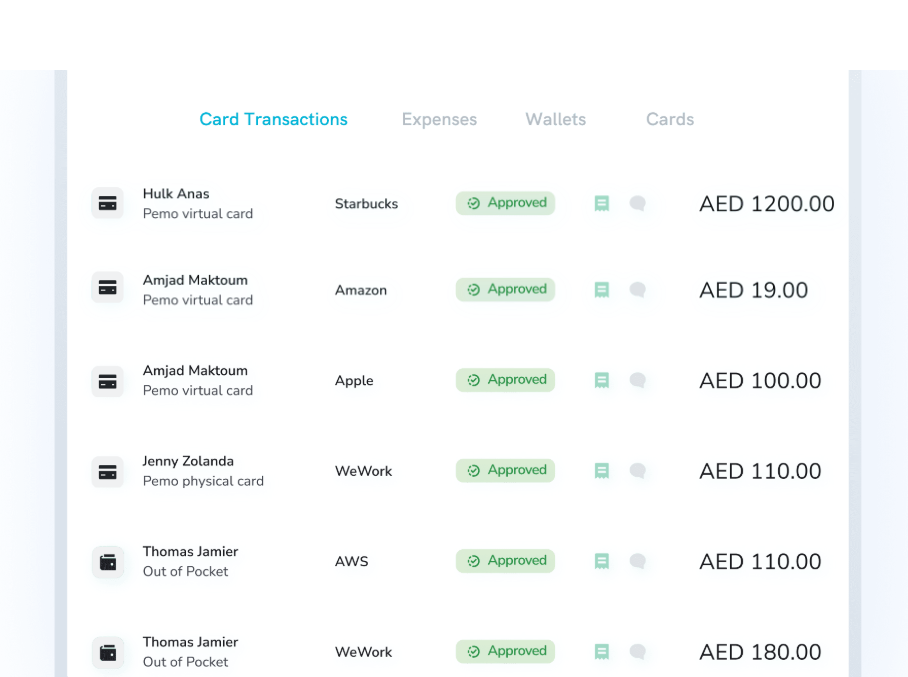

With Pemo cards, every transaction posts live.

Receipts get attached via mobile notification at the moment of purchase and Pemo's AI auto-matches them to the right transaction.

Your finance team sees what's spent the second it happens, and there's nothing to chase at month-end.

Here’s what this means for cash flow:

- No floating reimbursements sitting in payroll queues.

- No surprise expense submissions on the 28th of the month.

- Cash forecasts that reflect actual spending, instead of assumed spending.

Automated invoice management that protects your cash outflows

Pemo’s automated invoice management gives you control over when payments go out and visibility into what's coming up, which is usually impossible when invoices live in someone's inbox.

Our platform lets you collect, approve, schedule, and pay every invoice in one place.

The approval flow runs on whatever rules you set, so the right people see the right invoices without everyone being copied on everything.

Payments can get scheduled around your cash position, instead of being pushed out reactively when a supplier calls.

What this looks like in practice:

- A live payables dashboard shows every approved and pending invoice in one place, so you know exactly what's leaving the account in the next 14 or 30 days.

- Custom approval workflows route invoices automatically. The marketing director sees marketing invoices. The COO sees anything over 50,000 AED. The CFO sees the strategic ones. Nobody wastes a morning forwarding emails.

The cash flow benefit is straightforward: you stop being blindsided by what's owed, and you can time payments so your bank balance doesn't dip below where it should.

Pemo's Pricing

Pemo has a free plan called Kickoff for up to 2 card users, which gets you unlimited virtual cards, the mobile app, expense reports, card spending limits, and Excel exports.

To unlock the full petty cash and accounting features, you'd move onto one of our 2 paid plans:

- Essential: Starts at AED 29/month per card user. Adds cashback on online ad spend, direct accounting integrations, spend analytics, and customisable approval workflows.

- Business+: Custom pricing starting from 20 card users. Adds higher cashback rates, custom onboarding, a dedicated CSM, and priority support.

Want to learn more? You can sign up for Pemo's free plan or book a demo to see it in action.

Try Pemo for free

UAE cash flow management is fundamentally about closing one specific gap: the time between when money is spent and when finance finds out.

Most other problems trace back to that.

You don't fix it with spreadsheets or stricter policy memos.

You fix it with a system that captures every transaction at the source. Cards that enforce limits before the spend happens and receipts that match themselves to transactions.

Pemo is built for exactly this.

- Prepaid virtual corporate cards stop overspending at the source.

- Automated expense capture removes the month-end receipt chase.

- Invoice automation gives you real control over outflows.

- And accounting sync keeps your books current to the day.

If you're a UAE SME spending 8 to 10 hours a month reconciling expenses and still feeling like you're flying blind on cash, that's the problem worth solving this quarter.

You can sign up for the free Kickoff plan or book a demo to see why over 10,000 businesses across the MENA region run on Pemo.

FAQs

What's the difference between cash flow and profit?

Cash flow is the actual money moving through your bank account. Profit is what's left after revenue minus expenses on the accounting books.

You can be profitable and still run out of cash.

If your customers are slow to pay and your suppliers expect payment upfront, your books might show a healthy margin while your bank account hits zero.

How often should I review my cash flow?

Weekly at a minimum, ideally daily with a real-time dashboard.

A monthly review can be too slow.

By the time you spot a problem at month-end, the window to fix it might have already closed.

Weekly reviews catch trends, but daily dashboards can catch incidents while you can still act on them.

What's a healthy cash flow buffer for a UAE SME?

A common rule of thumb is to keep enough liquid reserves to cover several months of operating expenses, with extra room set aside ahead of corporate tax obligations.

The buffer itself isn't a legal requirement, but the corporate tax filing deadlines are, and FTA penalties for missing them can stack up over time.

Building cash aside through the year is how you avoid scrambling when the bill lands.

Can corporate cards really improve cash flow?

Yes, because they largely replace the reimbursement model and let you set spend caps before money actually leaves the account.

You control the budget at the point of transaction, instead of when reviewing receipts four weeks late.

For most UAE SMEs, that single change can remove a meaningful chunk of the monthly cash drift that nobody can otherwise explain.

Does Pemo integrate with the accounting software I already use?

Pemo integrates with QuickBooks, Xero, Zoho Books, Wafeq, and Tally, plus offers CSV exports for other platforms.

Online integrations sync card transactions and invoice payments into your accounting system through a review-and-export workflow, so your accountant skips manual data entry on every transaction.