Most UAE SMEs treat cash flow as something to react to.

A supplier chases payment, payroll lands, the VAT return comes due, and a slow client still hasn't paid. Then the scramble starts.

I've worked with profitable founders who couldn't explain why the account was nearly empty in the middle of their best sales quarter.

The profit was real. The cash had a timing problem, and nobody had been watching the calendar.

Cash flow optimization is the fix, which is a handful of deliberate moves that put money where it needs to be before anyone asks for it, so a tight Tuesday never becomes a missed payroll.

This guide covers six strategies a UAE finance lead can run in 2026, and where Pemo's cards and spend software make each one easier.

TL;DR

- Cash flow optimization means staying ahead of your cash position, so a squeeze shows up while you still have room to fix it.

- Forecasting is the first lever, and a rolling 90-day view can turn guesswork into something you can act on weeks early.

- The cash conversion cycle decides whether money reaches your account before it has to leave it, so tightening collections and timing supplier payments matters more than revenue alone.

- Pemo is the best platform to optimize your cash flow in the UAE, as it captures spend live, holds card budgets before money moves, automates invoice timing, and returns cashback that trims net outflow.

What does cash flow optimization mean for a UAE SME in 2026?

Cash flow optimization means managing the timing of money in and out so your business always holds enough working capital, with a buffer set aside for tax.

Timing is the important factor here.

Your company can look profitable on its P&L and still miss payroll, because profit is an accounting result while cash is whatever is in the account on the day a payment clears.

In the UAE, that gap bites harder than in many other markets.

Client payment terms can run long here, and credit for younger SMEs is hard to come by. Costs in Dubai and Abu Dhabi also keep moving whether or not your invoices have cleared.

Cash flow optimization comes from a few habits run together, each one keeping the account a step ahead of what it owes.

What are the most effective cash flow optimization strategies for UAE SMEs in 2026?

Each of these strategies targets a different spot where cash quietly leaks.

➡️ I’ve decided to frame them as questions so that it’d be easier for you to understand.

You can start with a spreadsheet, though a couple get much easier with the right tools:

How far ahead can you really see your cash?

Far enough that a slow client today doesn't blindside you in eight weeks.

If I could get every founder to build one habit, it would be this one.

That means a rolling 90-day cash forecast, a week-by-week view of expected money in and committed money out, updated as reality changes.

You want to start with what you know:

- Confirmed receivables and their realistic pay dates, payroll, rent, loan repayments, recurring subscriptions, and any tax falling due in the window.

- Then add the soft stuff: pipeline deals weighted by how likely they are to close, and variable spend like ad budgets or travel.

You re-forecast every week, which is the whole point of the word ‘rolling’, so the picture never drifts more than a few days out of date.

Two scenarios are usually enough: a base case, and a stress case where your largest client pays 30 days late and a deal slips.

If the stress case dips below your comfort line in week six, you've got six weeks to act.

You also want to pull forward a collection or delay a discretionary purchase before the gap becomes urgent.

The truth is, forecasts only work if the numbers feeding them are current, which is the part most SMEs get wrong.

If half your spending only surfaces at month-end, your week-three forecast is fiction.

This is why live transaction data keeps the model honest and why real-time spend visibility makes the other five strategies easier to run.

Are you collecting faster than you're paying out?

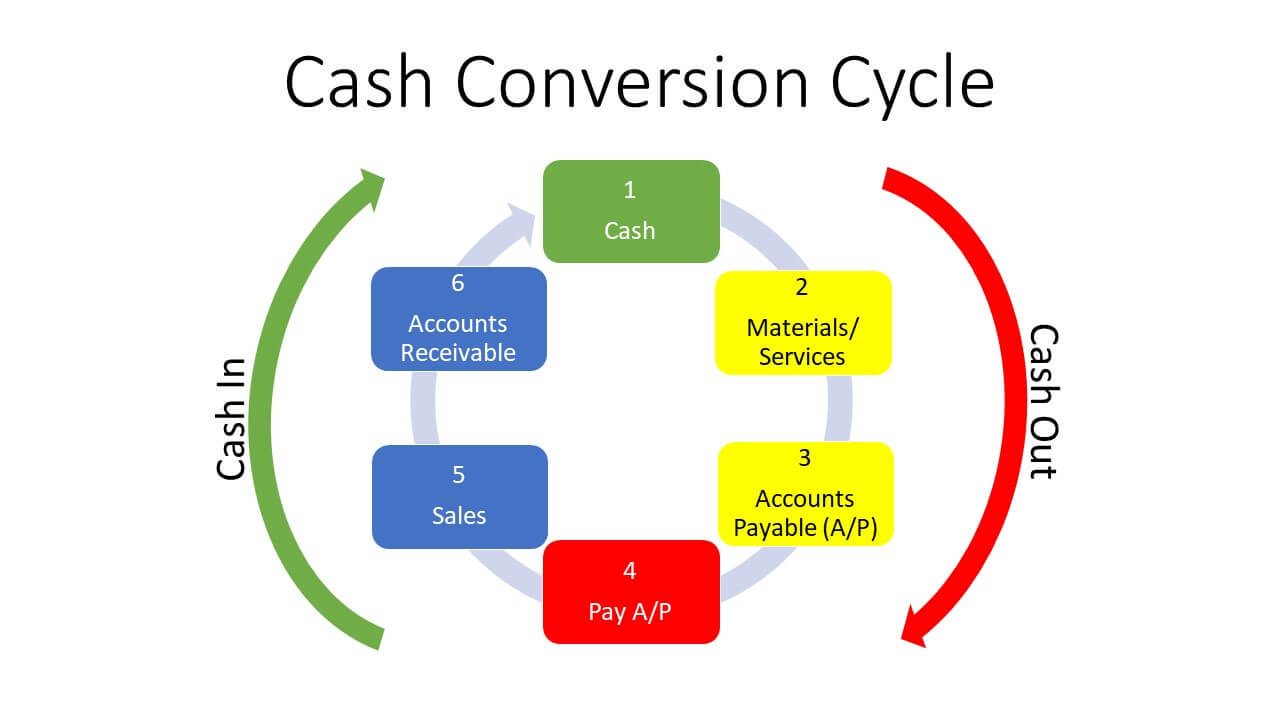

If you're not, you're funding the gap from your own reserves, and that gap has a name: the cash conversion cycle.

It's the number of days between paying your suppliers and collecting from your customers.

The wider it runs, the more working capital you have to float just to keep operating.

Two levers move it. You want to start with collection speed:

- Send the invoice the day the work is delivered. Waiting for a monthly billing run just adds days you can't afford.

- Ask for a deposit on larger jobs so you aren't bankrolling the whole project before a dirham comes in.

- Make paying you frictionless, with clear terms and a payment method on the invoice itself.

In a market where 60 and 90-day terms are normal, trimming even a week off your average collection time frees up cash you can feel.

The second lever, payment timing, gets its own strategy below, since deciding when to pay each supplier deserves more than a passing line here.

For now the principle holds: you want to collect early and hold your own payments to their full term, and the days in between start to shrink.

Is your spend planned or just discovered later?

For most SMEs, it's discovered later, which is exactly what makes outflows so hard to forecast.

When employees pay on personal cards and claim it back, or share one company card with no limits, finance only learns what was spent after it's gone.

The forecast you built on Monday is wrong by Wednesday.

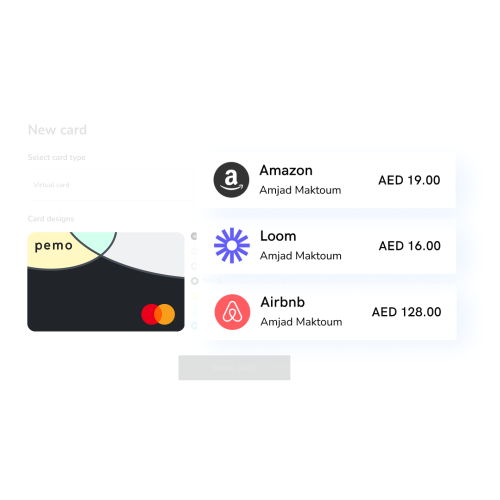

Planned spend works differently. You decide each team's budget up front, and the system holds them to it.

Prepaid corporate cards change that maths.

With Pemo (that’s us), you issue a virtual card to anyone who needs to spend and load it with a set budget, say AED 4,000 a month for whoever runs your paid social and search.

The card declines anything over that amount. So the budget holds on its own, with no awkward month-end conversation about who overspent.

A few controls make this practical:

- Hard caps per card: Set a ceiling per transaction, day, week, month, or year, and any charge above it is declined on the spot.

- Category and vendor locks: Tie a card to specific merchant categories or vendors, so an ad-spend card won't go through at a furniture shop.

- Freeze on demand: Pause or reactivate a card from desktop or mobile in seconds, with no bank call involved.

- Disposable single-use cards: Spin up a one-off card for a single purchase that expires after it's used, handy for a trial you don't want quietly renewing.

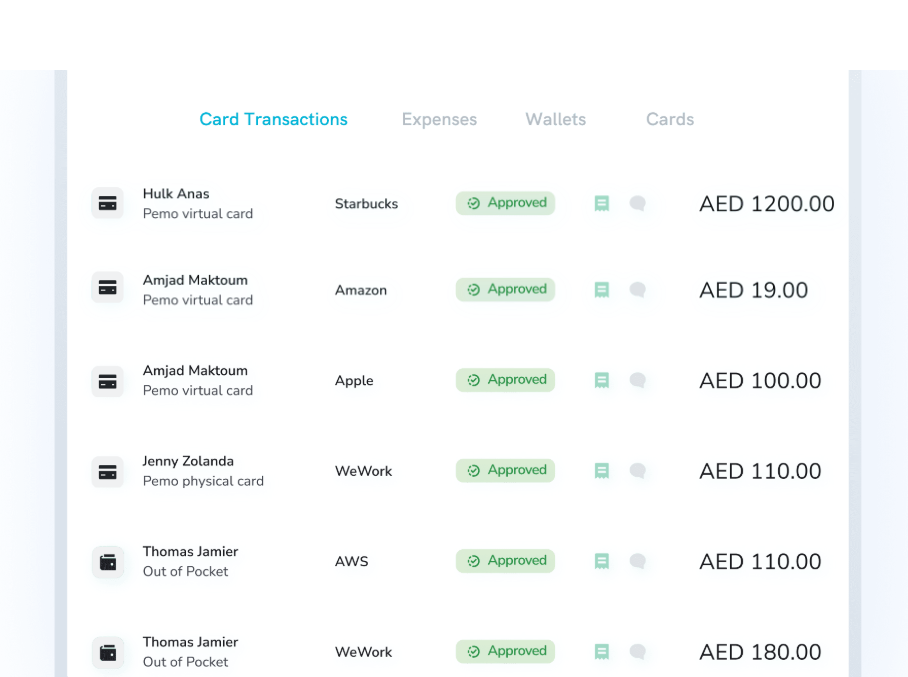

On the cash flow side, budgeted spend and real spend start to line up.

When every card carries a ceiling, the total your team can spend this month is a number you set, which makes it a number you can forecast.

Our cards work with Apple Pay, Google Pay, and Samsung Pay too, so nothing has to ship before a new hire can start spending inside their limit.

And the leakage that hides in unplanned spend, the duplicate SaaS tool or the annual renewal nobody flagged, gets caught early because every charge shows up live.

When should you pay each supplier?

Ideally, as late as the terms allow, and not a day later, with payment scheduled around your cash position.

Paying every bill the moment it arrives feels responsible, but it quietly drains your buffer.

If a supplier gives you 30 days, using all 30 keeps that cash working in your account for a month, ready for payroll or the next VAT bill if the timing turns tight.

Most of the skill is in sequencing. Some payments are fixed on date, like payroll and rent. Others carry flexibility.

When cash is tight in a given week, you want to prioritize paying the critical ones on time and push the flexible ones to the following week, once a client payment has cleared.

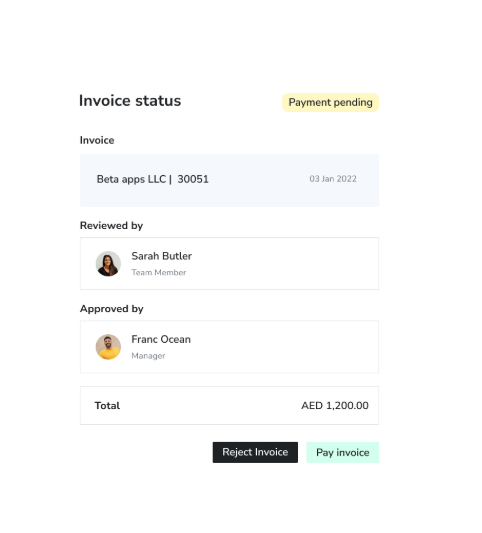

However, doing this from an inbox full of PDF invoices can break down fast.

Due dates slip, and bills get paid early by accident, with no single view of what's leaving the account and when.

Pemo's invoice management pulls every bill into one queue where you can approve and pay on a schedule you set.

You’ll be able to see exactly what cash is coming in, what's going out, and what's queued up for payment over the coming weeks.

You can also set up approval rules to send each invoice to the right person on their own, so a large bill goes straight to whoever signs off at that level without the whole team being copied in.

Have you set cash aside for tax before it's due?

If the answer is no, the UAE corporate tax regime has built a cash flow ‘trap’ with your name on it.

As of June 2026, corporate tax applies at 9% on taxable income above AED 375,000, with the return and the payment both due nine months after your financial year ends.

For a business closing its books on 31 December 2025, that deadline is 30 September 2026.

Timing is what turns a known cost into a crisis.

Tax builds up across the whole year as you turn a profit, but the bill lands as one payment months after the year closes.

A business that hasn't been setting cash aside finds itself needing a large sum at a single moment, often after the money has already been spent.

There's a second layer that catches people.

The VAT you collect from customers at 5% isn't yours to keep.

You net it against the VAT you've paid on your own purchases and hand the difference to the government each quarter or each month, so treating the collected cash as spendable is one of the easier ways to come up short when the return falls due.

The FTA has sharpened enforcement through 2026, with a restructured penalty framework and risk-based audits.

Building a buffer through the year is the cheapest insurance against all of it.

So you’ll need to treat tax as a recurring monthly outflow in your forecast, the same as rent or payroll.

You can estimate your annual liability and divide it across the months, then move that share into a separate reserve as you go.

By the time the deadline arrives, the cash should already be there.

This gets easier when your books are current.

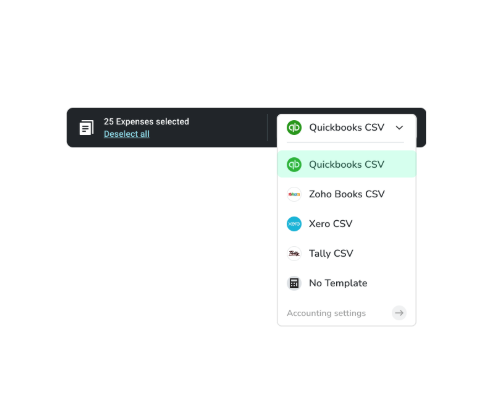

Pemo captures and categorises every transaction with its VAT treatment as it happens, then syncs to QuickBooks, Xero, Zoho Books, Wafeq, or Tally through a review-and-export step, so your taxable position stays visible through the year, well before filing season.

Knowing the number early is what lets you set the right amount aside.

Could your spending be paying you back?

Some of it can, through cashback and supplier discounts that lower what you spend on a net basis.

Small effect, but it compounds.

Spend you can't avoid, like advertising and software, can come with a percentage back.

On a meaningful monthly ad budget, even a modest rate can return a few thousand dirhams a year that would otherwise be gone.

Pemo builds this in.

Our platform offers cashback up to 2% on corporate transactions, including advertising (Google and Meta), foreign exchange (FX) fees, travel (like Booking.com), and fuel via CAFU.

That money lands back in the business, quietly lowering the real cost of spend you'd committed to anyway.

There's a softer version of the same idea in supplier and platform discounts.

Negotiated rates on the tools and travel you book anyway chip away at outflow without changing your spending at all.

None of these is a strategy on its own.

Stacked across a year of normal spending, though, they move the number.

What ties this to cash flow, beyond cost, is that every dirham returned is a dirham you don't have to fund out of receivables.

It's a small inflow on spend you'd already planned.

Sign Up For Pemo For Free

Picture your next quarter-end.

The forecast on your screen matches the balance in the bank, because every card transaction landed in the dashboard as it happened.

The tax money is already set aside, untouched.

Supplier payments are scheduled against receipts you can watch landing, and the marketing card stopped at its limit three weeks ago without a single message to finance.

It's the version of cash flow where you're ahead of the money, not chasing it.

Pemo gets you there by capturing spend at the source, holding budgets before money moves, automating your invoice timing, and keeping your books current to the day.

And over 10,000 businesses across MENA already run on it.

You can sign up for the free Kickoff plan, or book a demo to see it in action.

FAQs

What's the difference between cash flow management and cash flow optimization?

Management is keeping track of money in and out so you don't run dry.

Optimization goes a step further by improving the timing on purpose, so cash arrives before it has to leave, and a buffer is always in place.

How do I calculate my cash conversion cycle?

You can calculate your cash conversion cycle by taking the average days it takes to collect from customers, adding the days your inventory goes unsold if you hold any, and subtracting the average days you take to pay suppliers.

A lower number means cash returns to you faster.

For a service business with no inventory, it's mostly collection days minus payment days.

Can I forecast cash flow without expensive software?

Yes, a spreadsheet covers the basics, a week-by-week grid of expected receipts and committed payments for the next 90 days.

What makes or breaks a simple forecast is the quality of the data feeding it.

If your spending only becomes visible at month-end, the forecast is stale before you finish building it.

Live transaction data, from corporate cards or a spend platform, is what makes a forecast reliable.

Does improving your cash flow mean paying suppliers late?

No, it means paying on the terms you agreed and using the full window without going late.

Paying on day 30 of a 30-day term is good cash management.

Paying on day 45 is a late payment that strains the relationship and can cost you priority or pricing later.

You're using the full time you've been given, while keeping the relationship intact.

⚠️ Disclaimer: This article was last updated on the 26th of June, 2026, and if there's any misinterpretation of the information, please contact us, and we will fact-check it. This is not legal or accounting advice, so always consult with a qualified professional before making decisions.