This guide covers how to run a cash float properly in 2026, and the point where it quietly stops being worth the trouble.

TL;DR

- A cash float is a fixed amount of petty cash that an office keeps on hand for small in-person buys, then tops back up to that same amount on a set schedule.

- Run well, a float needs one named custodian, a per-purchase cap, a same-day log, a receipt for every withdrawal, and a count against the book on a regular cadence.

- It weakens once more people start dipping into it, when slips go missing and the count slowly drifts away from the written book.

- The modern swap is a corporate card drawing from one funded company wallet, which keeps the speed of cash while logging each purchase on its own.

- Pemo replaces the float with corporate cards funded from a central wallet, AI receipt matching, and direct sync to QuickBooks, Xero, Zoho Books, Wafeq, and Tally.

What is a cash float, and why do UAE businesses still rely on one?

A cash float is a fixed sum of petty cash that an office keeps available for small, everyday purchases that are awkward to put through a bank transfer or a card.

The idea is simple.

You decide on a set amount, let’s say AED 2,000, and keep it in a locked box with one person responsible for it.

People draw from it for taxis, couriers, a box of pastries for a client meeting, parking, or a quick run to the stationery shop.

At the end of the cycle, you total the receipts, add the cash left in the box, and the two should land back at AED 2,000.

You then top it up by exactly what was spent.

Accountants call this the imprest system, and it has been the backbone of small office spending in the UAE for a long time.

It sticks around for good reasons, since a lot of UAE spending is still small and cash-based.

Cards can still get declined at the smallest merchants, and a bank transfer can be an overkill for an AED 15 errand.

A float, meanwhile, costs nothing to set up. For a team of four or five, none of that is a problem worth solving.

How do you set the right cash float amount?

You want to set the float to cover roughly two to four weeks of small cash spending, and not a dirham more than that.

- Too high and you've got idle company money locked in a drawer, which is both a security risk and a waste.

- Too low and you're topping it up every few days, which defeats the point of having a float at all.

The cleanest way to size it is to look at it backwards: pull the last two months of small cash purchases and work out what the office spends in a typical week.

Then multiply that by the length of your top-up cycle.

If the team spends about AED 500 a week and you replenish every two weeks, a float of around AED 1,000 to AED 1,200 gives you a small buffer without leaving too much cash exposed.

I’d recommend that you write that number down as the official float amount and treat it as fixed.

The whole imprest method falls apart the moment the float amount becomes a moving target.

Who should hold and manage the cash float?

One named person should hold the float, and that same person should be the only one putting their hand in the box. This is the custodian.

Giving the float to a single custodian does two things:

- It makes one person accountable for the balance.

- It stops the box from turning into a free-for-all where four people take cash, and nobody quite knows the total.

The second principle matters more, and small UAE businesses skip it constantly.

Whoever guards the box shouldn't also be the one who approves its top-ups and checks the count.

Split those two jobs, and you catch the honest slip-ups as easily as the dishonest ones.

In a tiny team, that might mean the office manager holds the float while the finance lead or owner reviews and replenishes it.

What does a proper cash float log look like?

A proper cash float log records every withdrawal at the moment it happens, with the date, the amount, what it was for, who took it, and the receipt stapled or scanned in.

The format is less important than the discipline. A ruled notebook can work.

A shared spreadsheet works better, as it’ll timestamp entries and total the column for you.

What matters is that someone fills it in the moment cash leaves the box, while the detail is still fresh.

A workable log has a column for each of these:

- Date: the day the cash left the box, logged then and there.

- Amount: the exact figure taken, matched later against the receipt.

- Purpose: what the money was for, specific enough that nobody has to guess later. A line like "courier to JAFZA" beats a vague "office."

- Person: who took the cash and is answerable for the receipt.

- Receipt reference: a number or a photo link, so the slip and the line are tied together.

- Running balance: what should be left in the box after this entry.

You want to keep the running balance visible.

The day it stops matching the cash you can physically count is the day you've caught a problem early, which is the whole point.

How does cash float replenishment work?

Replenishment tops the float back up to its fixed amount by putting back exactly what was spent, supported by receipts.

The mechanics are straightforward.

At the end of your cycle, you count the cash left in the box and add up all the receipts collected.

Those two figures together should equal your fixed float amount.

If your float is AED 2,000 and you're holding AED 350 in cash plus AED 1,650 in receipts, you replenish with AED 1,650 to bring the box back to AED 2,000.

That top-up is also the moment your bookkeeping happens.

You don't post twelve tiny journal entries through the month.

You post the expenses once, at replenishment, categorized against the receipts, and reimburse the float in a single transfer.

Two things make replenishment go wrong that I’d recommend you watch out for:

- Replenishing without matching receipts, which lets unsupported spending slip through.

- Replenishing to a number other than the fixed float, which breaks the imprest logic.

How do you reconcile and audit a cash float?

Reconciling a cash float means counting the physical cash and the receipts, then checking that the two together add up to the float amount.

For an active float, you can do this weekly.

A weekly count keeps any gap small and recent enough to investigate, while a gap you find after 30 days is usually impossible to trace to a cause.

The count should be done, at least some of the time, by someone other than the custodian.

A surprise count by the finance lead or owner, once in a while and unannounced, can do more for control than any written policy.

When the numbers don't match, the difference tells you something specific:

- Cash short with receipts to cover it usually means a withdrawal went unlogged.

- Cash short with no receipts is the one that needs an internal investigation into what happened.

This is why you want to keep every count and every signed-off replenishment on file.

What controls keep a cash float from leaking money?

The controls that matter most are a hard per-purchase cap, a strict no-receipt-no-reimbursement rule, surprise counts, and a clear split between who spends and who reconciles.

Petty cash rarely leaks in big, obvious ways.

It goes in small, forgettable amounts that nobody questions on a busy afternoon.

A AED 80 taxi that never made the log or a top-up approved without anyone matching the slips to the total.

A few controls catch most of it before it adds up:

- A per-purchase cap: set a ceiling, say AED 200, above which a purchase can't come out of the float at all and has to go through proper procurement.

- No receipt, no reimbursement: make this rule absolute, so the float can't be used to wave through vague or unsupported spending.

- Surprise counts: an occasional unannounced count by someone other than the custodian keeps everyone honest and catches drift early.

- Separation of duties: the person spending shouldn't also be the one approving and reconciling the same float.

Where does cash float management start to break down?

A cash float breaks down at the point where the number of people touching it outgrows the one person trying to track it.

The truth is that it rarely fails all at once.

It starts with a single rushed week, when two people grab cash for a delivery and a client run, and neither writes it down until later.

The count comes up short on Thursday, so the custodian backfills the log from memory and rounds a little to make it balance.

And the CFO who wanted clean numbers at the start of the month is still missing the petty cash figure two weeks later.

What's the modern alternative to running a cash float?

The modern alternative keeps the float's convenience and removes the cash entirely, by giving each person who used to draw from the box a corporate card that pulls from one funded company wallet.

The category is called spend management, and it lines up with the cash float idea almost piece by piece.

Here’s how it works:

- The funded wallet is your float.

- Each card's limit does the job of the per-purchase cap.

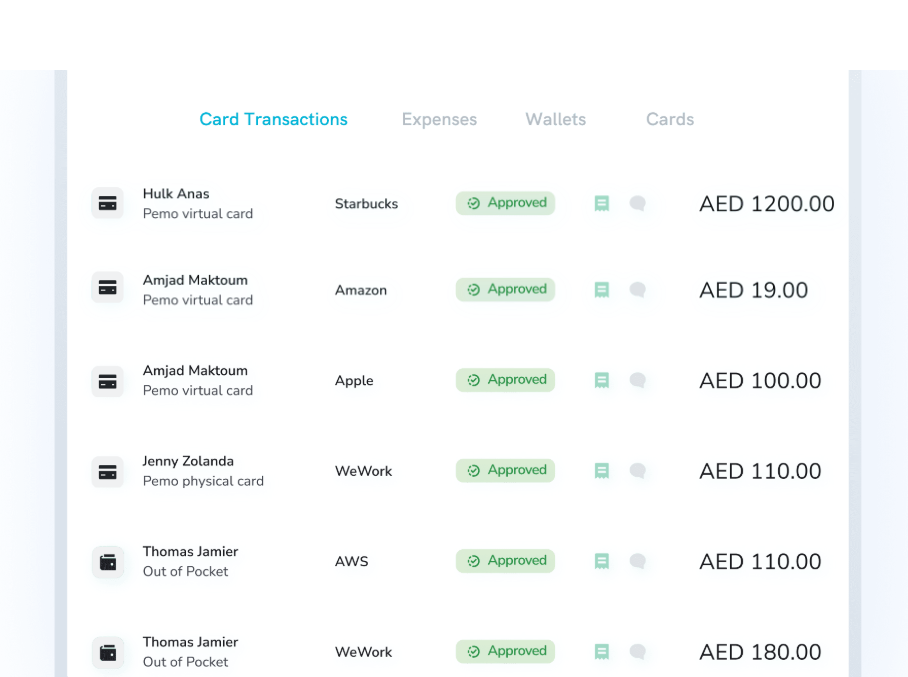

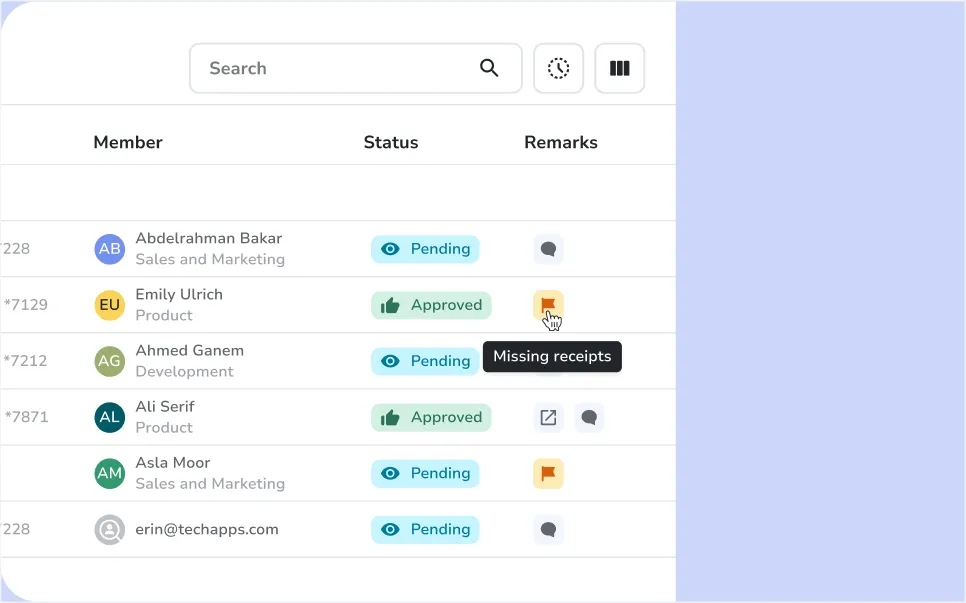

- The transaction log writes itself where you used to keep a notebook, and the receipt gets photographed the moment it's handed over.

The one real change is timing.

All of it happens the second a card is used, with nobody writing anything down by hand.

Pemo (that’s us) is one of these platforms, built specifically for UAE businesses.

Our platform turns a cash float into a set of corporate cards funded from one company wallet, so you keep the speed of cash and lose the part where someone counts a tin.

You can hand a card to anyone who used to take cash from the box in seconds, from the dashboard, with no bank form and no wait.

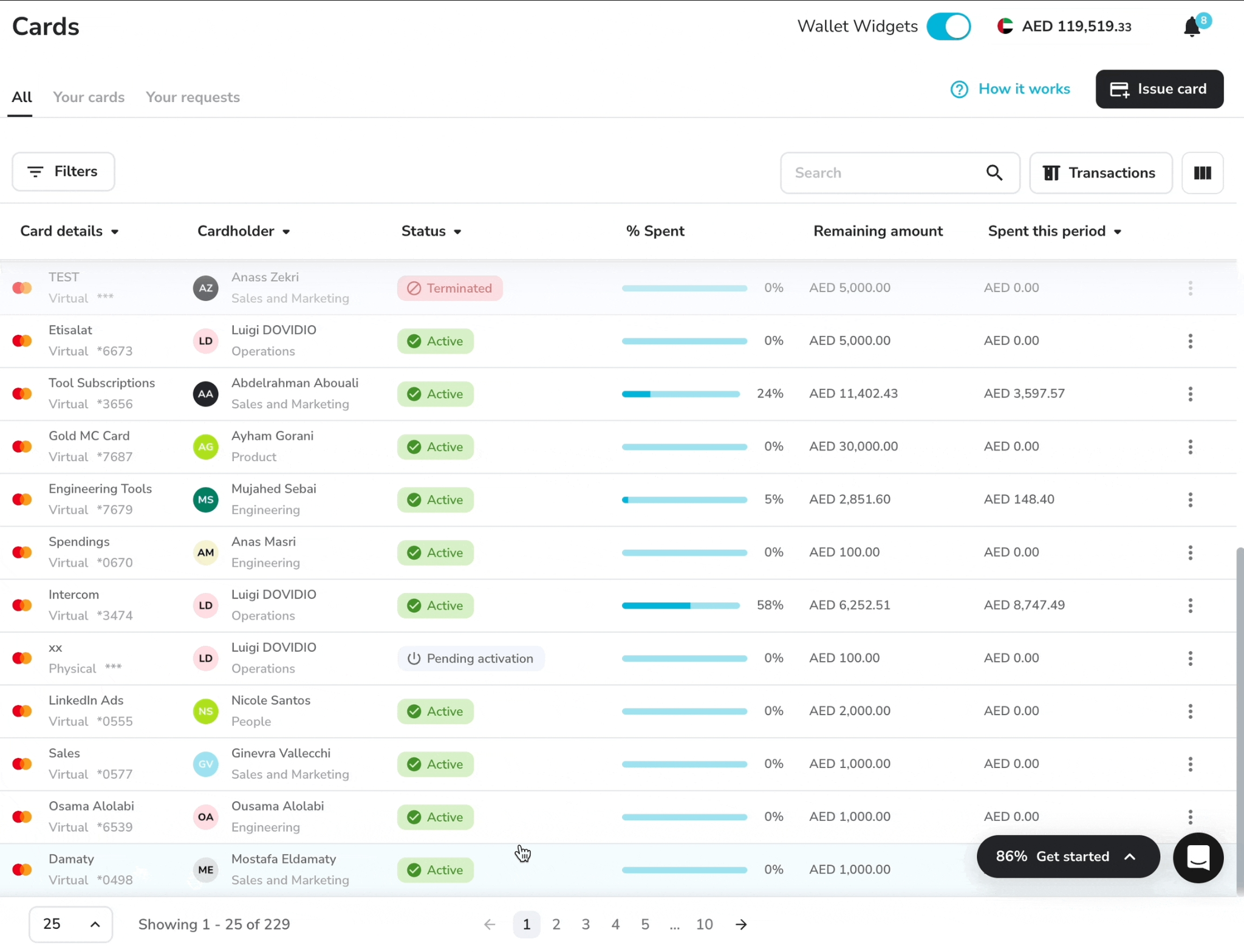

Each card comes with its own guardrails:

- A spending cap per card, by transaction or by day, week, month, or year, so the limit fits the person and the job.

- Category locks, so a card set up for fuel won't go through at an electronics shop.

- A freeze switch on a desktop or mobile, useful the day a phone goes missing or someone hands in their notice.

- Single-use cards, created for one purchase with a set amount, are gone the moment that payment clears.

For the rare moments cash truly can't be dodged, an ATM run or a merchant still stuck in the cash-only era, there are physical cards too, and everything online runs on unlimited virtual ones.

More than 10,000 businesses across the MENA region use it, and plenty of them came over after a petty cash setup buckled under a growing team.

And the best part? A card setup like this isn't only for big teams.

A two-person company can run it on a free tier, and a hundred-person company can run it with proper approval chains and departmental budgets, off the same setup.

How do you transition from a cash float to Pemo?

You move off a cash float by winding it down over a short, deliberate transition, so nothing breaks along the way.

The float doesn't need a dramatic shutdown.

It needs a clean close:

- Stop replenishing the float: You can set a final date after which the box gets no more top-ups, so the cash balance only goes down from here.

- Issue cards to the people who held cash: Give each former cash-taker a Pemo card, and set the limit to match the cap they were effectively working under before.

- Match the rules to your old controls: The per-purchase cap becomes a card limit, and the approved-merchant idea becomes a category restriction. The surprise count becomes a live feed you can open at any time.

- Run one final reconciliation: Count the cash, total the last receipts, post the final expenses, and sign the float off to zero with a closing record on file.

- Close the box: Bank the remaining cash, retire the notebook, and keep the historical log with your VAT records for the five-year retention window and seven for corporate tax.

Most of your everyday spending shifts to cards almost immediately.

The handful of edge cases where cash is genuinely the only option can stay on a single small float, sized right down, with the same controls you've just learned.

Sign Up For Pemo For Free

Running a cash float well rests on a short list of habits.

Get those few right, and a float can work: one custodian, a fixed amount, a per-purchase cap, a receipt for every withdrawal, a same-day log, and a regular count by a second pair of eyes.

The hard part is that every one of those habits depends on a person remembering to do something manual, on a busy day, every single time.

The method quietly fails right there, which is why most UAE businesses eventually move the float onto cards.

A funded wallet and a card for each person hold those same principles in place, and they do it on every transaction without anyone needing a reminder.

The cap becomes a card limit, and the log keeps itself. By the time your accountant logs in, the reconciliation is already done.

You can sign up for the free plan or book a demo to see it in action.

⚠️ Disclaimer: This article was last updated on the 26th of June, 2026, and if there's any misinterpretation of the information, please contact us, and we will fact-check it. This is not legal or accounting advice, so always consult with a qualified professional before making decisions.