In 2026, picking a corporate card for your UAE SME isn't really about picking a card. It's about picking a platform.

The plastic (or virtual number) is just the entry point. What actually matters is the software that sits behind it: how it controls spend, how fast it issues new cards, how deeply it connects to your accounting stack, and whether it can replace the manual work your finance team is drowning in.

Whether you're a growing business in Dubai or a finance team managing multiple departments across the UAE, this guide will help you compare the best corporate card options available right now and choose the right one for how your business actually works.

TL;DR

- Pemo is the best all-in-one corporate card and spend management platform for UAE SMEs, with a free plan, AED 29/month pricing, accounting automation, and direct integrations with QuickBooks, Xero, Zoho, and Tally.

- Regional fintechs like Xpence are strong options for teams that want modern dashboards, AI-powered analytics, and rewards programs, though pricing and feature depth vary widely.

- Traditional bank cards from HSBC, Emirates Islamic Bank, and FAB offer high credit limits and global acceptance, but come with minimal software tools and slow onboarding processes.

What to look for in a 2026 corporate card (hint: it's not the plastic)

In the past, corporate cards were issued by banks, used for travel and procurement, and manually reconciled weeks later.

That world is gone.

When I evaluate corporate cards for SMEs in the UAE, I look past interest rates and card materials entirely. Here's what actually determines whether a card saves your finance team time or creates more work.

#1: Software and integration depth

Does the card come with a real spend dashboard? Not a basic transaction history, but an actual platform that lets you see spending patterns across departments in real time.

Can you connect it to your accounting software? I'm talking direct sync with QuickBooks, Xero, Zoho, or Tally, where transactions flow automatically into the right accounts. If not, your finance team is stuck with manual exports and CSV uploads every month.

And can it categorize expenses on its own? The difference between a card that just records transactions and one that auto-codes them to your chart of accounts is hours of work every month-end.

#2: Real-time controls and limits

Modern finance teams need granular controls. Not just a monthly card limit set by the bank.

Can you block certain merchant categories? Can you set daily, weekly, or per-transaction limits? Can you freeze a card instantly from your phone when something looks off?

These aren't luxury features. For a UAE SME managing 10, 20, or 50 employees with cards, the ability to set rules before money is spent is the difference between control and chaos.

#3: Automation that actually reduces work

Does the card support receipt capture via mobile? Can it match receipts to transactions automatically using OCR or AI? Does it reduce manual reconciliation?

Without these, your finance team stays buried in paperwork at month-end. I've seen teams spend 3-4 full days just chasing missing receipts. A good corporate card platform makes that problem disappear.

#4: All-in-one platform vs. isolated features

Many cards offer isolated features. A dashboard here. A receipt scanner there. But the most effective systems combine cards, approvals, invoicing, and accounting sync in one place.

Ask yourself: is this just a card, or is it a spend management platform? Because in 2026, the card is the least interesting part of the equation.

Comparison: The best corporate card options for UAE SMEs in 2026

To help you decide, we’ve outlined three common options UAE businesses are considering in 2026: traditional banks, regional fintech players, and Pemo's all-in-one spend management platform.

Here's how they compare across the criteria that matter:

#1: Pemo's all-in-one spend management platform

If you want one platform that handles corporate cards, expense management, invoice payments, and accounting automation together, Pemo is the strongest option for UAE SMEs in 2026.

I'm putting Pemo first here because most corporate card decisions in the UAE come down to a simple question: do you want just a card, or do you want the entire financial workflow around it handled in one place? Pemo answers that question.

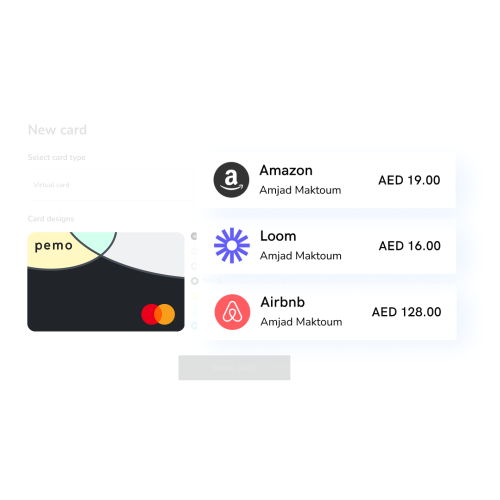

Corporate cards with rules built in

Every employee who needs to spend gets a Pemo card. Physical (Visa or Mastercard) or virtual, issued in minutes. Virtual cards are unlimited. Physical cards, one per person. Both work with Apple Pay, Google Pay, and Samsung Pay.

Here's what matters: you set the rules before anyone spends a single dirham.

Limits by amount (per transaction, daily, weekly, monthly, yearly). Limits by merchant category (allow SaaS subscriptions, block ATM withdrawals). Limits by vendor (this card only works at Google Ads). Limits by time (active only during business hours).

If someone tries to spend outside the rules, the transaction gets declined. No awkward conversations after the fact.

Need a one-time purchase? Create a single-use virtual card with an exact amount, use it, and it self-destructs. Useful for vendor payments where you don't want a recurring charge sneaking through.

Cards can be frozen instantly from the app. Lost your physical card at a conference? Frozen in two taps, replacement on the way.

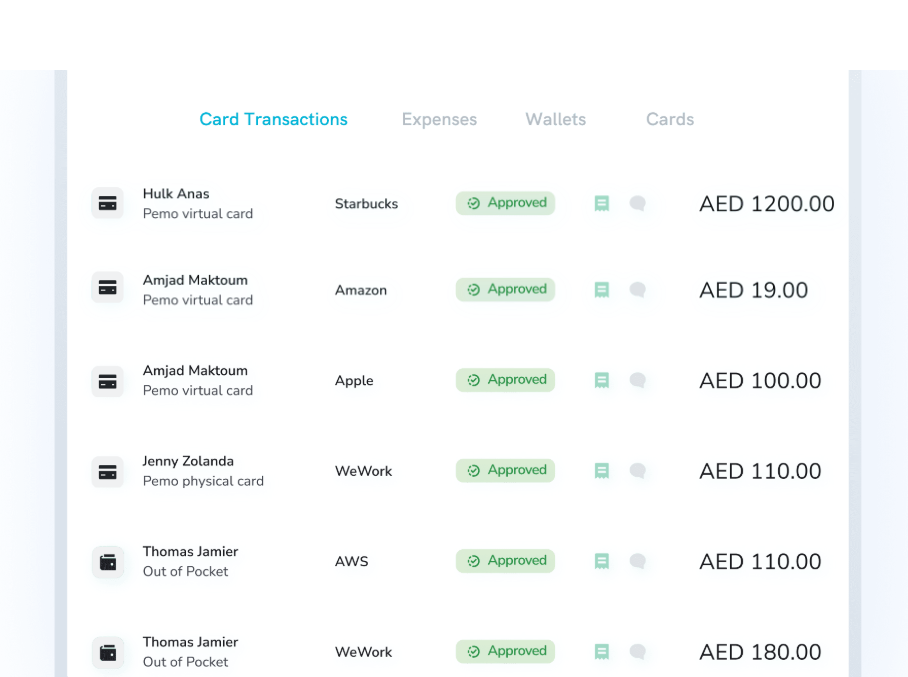

Expense management that runs itself

Every card transaction shows up in your dashboard the moment it happens. Not at month-end. Not when someone remembers to submit it. Immediately.

When an employee makes a purchase, they get a push notification asking them to snap the receipt. AI matches the photo to the transaction. If they forget, the system nags them and flags it for the finance team.

Out-of-pocket expenses get submitted through the app with the same receipt-capture flow and routed through approval workflows.

Multi-level approvals are configurable: marketing spend goes to the CMO, anything over AED 5,000 goes to the CFO, travel expenses route to the office manager. You set it once. It runs without you.

Expense reports generate themselves from the transaction data. No more month-end scramble where finance chases 30 people for missing paperwork.

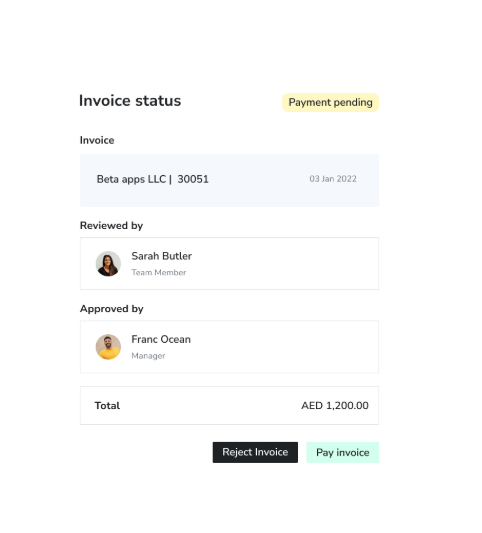

Invoice payments without the filing cabinet

This was actually Pemo's first product, and it shows. Vendor bills get captured using AI-powered OCR (photograph the invoice, the system reads it).

Each invoice routes through your approval workflow with a full audit trail. Once approved, pay directly from your Pemo account.

And Pemo helps you save on international transfer costs with lower fees than some competitors in the market.

Accounting automation

This is where Pemo pulls ahead of most alternatives.

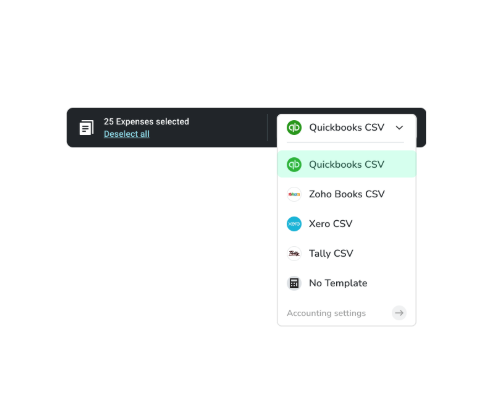

Transaction data flows automatically between Pemo and your accounting software. QuickBooks, Xero, Zoho, Tally, and others. Your finance team gets visibility into transactions instantly, synced in real-time.

Expenses are automatically categorized into your chart of accounts. That alone saves hours of manual coding every week.

Pricing

Pemo has a free plan for up to 2 card users that gives you access to unlimited virtual cards per user, a mobile app, expense reports, card spending limits, and Excel reports of expenses.

To access the advanced expense and accounting management features, you need one of Pemo's 2 paid plans:

- Essential: Starts from AED 29/month for 1 card user, which adds cashback on online advertising spend, integration with popular accounting platforms, spend analytics, and more.

- Business+: Custom pricing that starts from 20 card users, which adds cashback on card spending, custom onboarding and training, and a dedicated CSM.

Pros and Cons

✅ Free plan available.

✅ AED 29/month is the most affordable paid plan among UAE spend management platforms.

✅ Full AP automation, expense management, and accounting sync in one platform.

✅ Both Visa and Mastercard on a single platform, which means fewer declined transactions.

❌ Prepaid model only. No revolving credit. You need to load funds before spending, and wallet top-ups aren't available on weekends.

#2: Traditional bank business credit cards

If your main need is a credit line and global acceptance, and you're fine managing finances the old-fashioned way, traditional bank corporate cards still have a place.

But let's be clear about what you're getting and what you're not.

What banks do well

High credit limits. If your company qualifies, banks like HSBC, Emirates NBD, and First Abu Dhabi Bank (FAB) can offer significant credit lines that fintech prepaid cards simply can't match. For businesses that need to spend now and pay later, this matters.

Global acceptance is essentially guaranteed. These cards work at every POS terminal, every e-commerce checkout, everywhere.

Some banks offer travel perks, cashback programs, and loyalty rewards. Emirates Islamic Bank, for example, gives access to Mastercard's Smart Data tools for transaction reporting.

What banks don't do

This is the longer list.

No spend management software. No real-time dashboard that shows you who spent what, where, and why. No automated expense categorization. No receipt capture. No mobile app for approvals.

Card issuance takes days or weeks. You can't spin up a virtual card in 30 seconds for a new Google Ads campaign. You fill out paperwork, wait for approvals, and hope the timeline works.

Cards are often shared among team members. That means one card number floating around the office, OTPs going to the CFO's phone, and zero visibility into who actually made which purchase.

And reconciliation? Entirely manual. Your finance team downloads statements, matches them to receipts (if receipts exist), and enters everything into the accounting software by hand.

Key players

HSBC offers a virtual card platform where leaders can create single and multi-use virtual cards. It's a viable option for businesses handling large-value, high-volume payments to suppliers. But HSBC doesn't disclose its pricing publicly, so you'll need to fill in a questionnaire and wait for the bank to get back to you.

Emirates Islamic Bank offers corporate credit cards with virtual card numbers linked to a primary card. The virtual cards can be configured for single or multiple uses with specified transaction controls like amount and usage dates. The monthly profit share is 1.99% with AED 0 annual membership fee. But the user interface is outdated, and the pricing model based on monthly profit sharing isn't the most transparent.

FAB and Emirates NBD offer standard corporate credit card programs with the typical banking perks. Credit limits depend on company financials, and the application process involves documentation, credit checks, and wait times.

#1: Regional fintech corporate cards

The UAE has become a hub for fintech spend management companies over the past few years. If you want modern software, quick digital onboarding, and features like AI analytics or rewards programs, this category has real options.

But the quality varies. A lot.

Some of these platforms are genuinely strong products. Others are marketing-forward with feature depth that doesn't quite match the promise.

The verdict: how to choose the right corporate card for your business

Your choice depends on your business size, financial goals, and how much manual work your finance team can handle.

Choose a traditional bank card if your main need is a credit line and you have the internal resources to manage finances manually. Banks still win on credit limits and established trust.

Choose a regional fintech card if you're a fast-moving team that wants modern software, quick card issuance, and you can handle a bit of fragmentation in your finance tools. Pay attention to the specific platform you choose, because the differences between players are significant.

Choose Pemo if you want a connected, modern platform to manage every aspect of your financial operations: cards, invoices, expenses, and reporting, all in one place. Pemo stands out for UAE SMEs because it combines the deepest feature set with the most accessible pricing in the market.

The free plan lets you test everything before committing. And at AED 29/month per user on the Essential plan, it's a fraction of what most alternatives charge.

See Pemo's all-in-one platform in action

Ready to simplify spend control, automate your financial workflows, and get real-time visibility into every dirham your company spends?

See Pemo's all-in-one platform in action and discover how UAE SMEs are modernizing their finance operations with better tools, not more complexity.

Book a demo or sign up for free.

⚠️ Disclaimer: This article was last updated on 1st of May, 2026 and if there's any misinterpretation of the information, please contact us and we will fact check it.