Virtual cards exist only as digital details for online payments, physical cards are the plastic you tap in person and use at ATMs, and for most UAE businesses in 2026 the better question is not which one to pick but how to run both well.

In this guide, I’ll go over the difference between virtual and physical corporate cards, and where each of them makes sense.

TL;DR

- Virtual cards are created instantly and used online for things like advertising spend, software subscriptions, and one-off vendor payments, with tight controls and self-expiring single-use options.

- Physical cards cover in-person purchases and ATM cash, work through mobile wallets like Apple Pay and Google Pay, and arrive within about 72 hours.

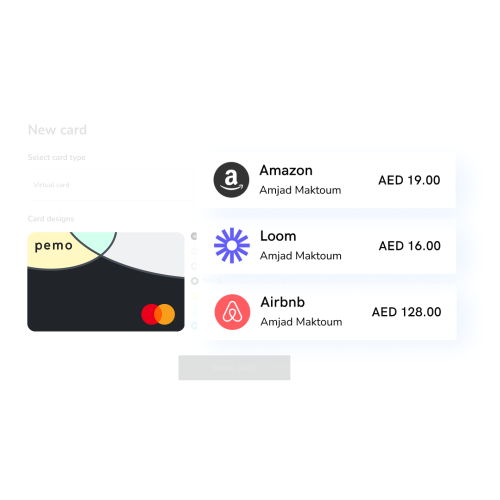

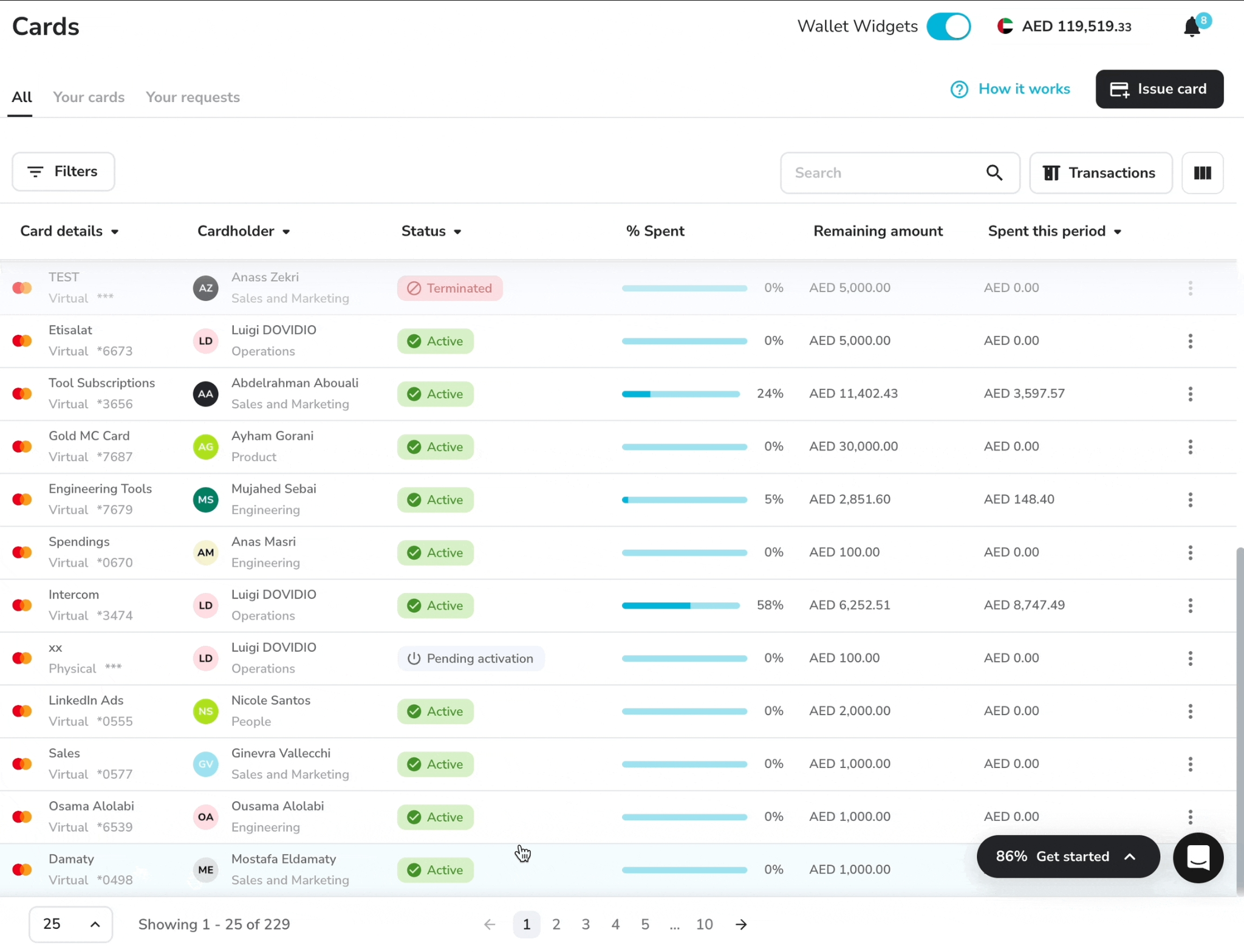

- Most UAE businesses need both, and Pemo issues virtual and physical Mastercard and Visa cards from one platform, with spend rules set before anyone pays and every transaction tracked automatically.

What's the difference between virtual and physical corporate cards?

The difference is the format: a virtual card is a set of card details you generate in software for online payments, and a physical card is plastic that also handles in-person purchases and cash.

Everything else follows from that one fact.

- A virtual card appears in your account the second you create it, with its own number, expiry date, and CVV.

- A physical card has to be manufactured and posted, which in the UAE can mean a couple of days.

The two also behave differently once they're in use.

You can lock a virtual card to a single vendor, cap it at an exact amount, or set it to close itself after one purchase.

A physical card is built for repeat use across shops, restaurants, and ATMs, so it gives up some of that surgical control in exchange for everyday convenience.

Here’s a side-by-side overview: 👇

What is a virtual corporate card?

A virtual corporate card is a card that exists only as digital details, with no plastic version, made for online and app-based business payments.

You generate it in a spend management platform like Pemo, and within seconds it has a working number and the security details behind it.

From there it behaves like any card online.

You can drop it into a checkout, add it to a mobile wallet, or hand a unique one to each vendor so a single leaked number never exposes the rest of your spending.

The appeal for finance teams is control.

A virtual card can be capped to the exact value of a purchase, restricted to one merchant, or issued for a fixed window and then closed.

If a number gets compromised, you can cancel it in a tap and create a replacement without anyone driving to a branch.

When does a virtual card make the most sense?

Virtual cards work best for spending that happens on a screen.

Recurring software subscriptions are a clean example.

You can give each tool its own virtual card with a monthly cap, and a surprise price hike or a free trial that quietly converts gets stopped at the source.

Online advertising is another strong fit. Marketing teams running Google Ads and Meta budgets can put each platform on its own card, so a misfired campaign can't silently drain the money meant for a different channel.

💡 Expense management solutions like Pemo also offer cashback on online advertising spend (e.g., Google Ads), as well as additional cashback on card spending, such as 2% cashback on FX fees.

What is a physical corporate card?

A physical corporate card is the plastic version of a company card, used for in-person payments and ATM cash withdrawals.

It works the way any card has for decades.

You tap it at a terminal or dip the chip, and pull cash when a supplier only deals in dirhams and a paper receipt.

The difference from a personal card is what surrounds it: the same spend rules, category limits, and live visibility a finance team applies to a virtual card travel with the plastic too.

When does a physical card make the most sense?

Physical cards are for the offline parts of running a business.

Think travel. Hotels that pre-authorise on a tap, taxis, a client dinner where you hand the waiter a card, and the odd merchant whose terminal still wants a chip and PIN.

Think cash. Site or event spend where a vendor wants notes, not a tap, is something only a physical card covers through ATM access.

For field teams and anyone facing customers in person, plastic stays the dependable option.

➡️ With Pemo’s physical corporate cards, you can still spend responsibly with pre-set limits and policies for every transaction.

Are virtual cards more secure than physical cards?

In most day-to-day situations, yes, a virtual card gives you more security, though the honest answer is that each format is safer in a different way.

Virtual cards cut your exposure.

A single-use card leaves nothing useful behind once the payment clears, and a vendor-locked card is worthless to anyone who steals the number.

If details leak, cancelling and reissuing takes seconds.

Physical cards carry the old risks of anything you can drop or have lifted from a pocket.

However, they’re good at pulling cash from an ATM, and paying at the terminals that still insist on a physical chip and PIN.

So the safer setup that we’ve seen work for most teams is to use virtual cards as the default for online spend and keep a physical card ready for the situations that genuinely need it.

Sign Up For Pemo For Free

Pemo offers an all-in-one expense management software for SMEs and growing businesses in the UAE, with pre-loaded corporate cards that can turn your transactions into a tracked, categorized, audit-ready expense.

Our virtual + corporate cards and AI software work together so your finance team stops chasing receipts, month-end reconciliation moves much faster, and your spending stays inside the rules you set before anyone swipes a card.

If you're looking for expense management software with smart corporate cards for your UAE-based team that offers:

- AI receipt matching and real-time spend visibility.

- Direct sync with QuickBooks, Xero, Zoho Books, Wafeq, and Tally.

- Cashback on Google Ads, Meta Ads, and FX fees.

- AED-denominated pricing that starts at 29 a month.

Then you can sign up for the free Kickoff plan or book a demo to see why over 10,000 businesses across the MENA region run on Pemo.

⚠️ Disclaimer: This article was last updated on the 19th of June, 2026, and if there's any misinterpretation of the information, please contact us, and we will fact-check it. This is not legal or accounting advice, so always consult with a qualified professional before making decisions.

Frequently asked questions

Do UAE businesses have to choose between virtual and physical cards?

No, I’d argue that treating it as a choice is a mistake.

Business spending doesn't split neatly into online and offline.

In a single week your team might renew a SaaS subscription, run an ad campaign, book a flight, take a client to dinner, and need petty cash for an event setup.

Can I use a virtual card for in-store purchases?

Yes, once you add it to a mobile wallet.

A virtual card on its own can't be swiped, but loaded into Apple Pay or Google Pay it taps at any contactless terminal, which covers most shops and restaurants in the UAE.

For chip-and-PIN-only terminals or for cash, you'll still want a physical card.

Can virtual cards be added to Apple Pay or Google Pay?

Yes. Pemo virtual cards work with Apple Pay, Google Pay, and Samsung Pay, so your team can pay by phone without carrying plastic.

The card details stay inside the wallet, which is one reason virtual cards are harder to skim.

Can I withdraw cash with a virtual card?

No, virtual cards don't support ATM withdrawals.

Cash access is one of the few things only a physical card handles, which is part of why most businesses keep at least one physical card in the mix.

On Pemo, ATM withdrawals cost AED 5.25 each.

What is a single-use virtual card?

A single-use virtual card is a virtual card that works for exactly one payment and then closes itself.

It's handy for a one-off supplier, a trial you don't fully trust, or any purchase where you'd rather the number couldn't be charged a second time.

You set the amount, make the payment, and the card expires.